Volume 1

The practical grocer : a manual and guide for the grocer, the provision merchant, and allied trades / by W.H. Simmonds ; with contributions by specialists, trade experts, and members of the trades ; illustrated by a series of separately-printed plates.

- Simmonds, W. H.

- Date:

- 1904

Licence: Attribution-NonCommercial 4.0 International (CC BY-NC 4.0)

Credit: The practical grocer : a manual and guide for the grocer, the provision merchant, and allied trades / by W.H. Simmonds ; with contributions by specialists, trade experts, and members of the trades ; illustrated by a series of separately-printed plates. Source: Wellcome Collection.

Provider: This material has been provided by The University of Leeds Library. The original may be consulted at The University of Leeds Library.

306/346 (page 248)

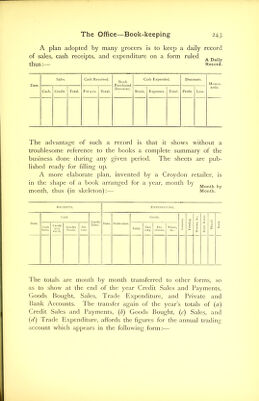

![thus described:—There should be sales checks for cash sales and others for credit sales. Each salesman should have a package or book of each kind of these checks. These checks should be simple, but each set of different form and colour, and should be printed “cash sale” or “credit sale”. The cash sale check should read something like this when made out by the clerk: Cash Sale: Salesman No. 6, 1 lb. Coffee, 28 cents. This check, with the money, should go to the cashier, who sends back the change, if any, and places the check on the spindle corresponding to the salesman’s number. In making up the cash, each salesman’s sales are footed up separately, and the total is entered under cash sales for the day. If a credit sale is made, the salesman makes out a check which is headed “ credit sale This may read: Credit Sale: Salesman No. 8, James K. Lane, 12 Main Street. (.Details follow.) These credit sales slips are used for entering up the accounts of the debtors, but no account is to be kept of credit sales Credit by individual salesmen. When the bills are paid, cash sups. saje s]jpS are to be ma(je by the cashier for each sales- man for the goods sold by him, and the same credited as his sales of the day on which they are paid. Only the amount, the salesman’s number, and amount of sale is necessary on such a slip. A set of double-entry books should be kept, consisting of a journal (i.e. a day book), cash book, and ledger. Everything is posted from the journal to the ledger. Besides these, a ledger is to be kept for accounts with customers. This is entirely inde- pendent of the double-entry books. A sale is not to be credited to merchandise account until it is paid. This ledger has drawn Credit Sale °ff upon it the items from the salesmen’s credit sale Checks. checks. An extra space gives salesmen’s numbers, otherwise the ruling is the regular ledger pattern. The checks are not destroyed, but are strung on a wire after the entry is made on the ledger. If for any reason the original credit sale check is needed for reference, it is easily found, for the checks are strung on](https://iiif.wellcomecollection.org/image/b21505949_0001_0306.jp2/full/800%2C/0/default.jpg)