Volume 1

The practical grocer : a manual and guide for the grocer, the provision merchant, and allied trades / by W.H. Simmonds ; with contributions by specialists, trade experts, and members of the trades ; illustrated by a series of separately-printed plates.

- Simmonds, W. H.

- Date:

- 1904

Licence: Attribution-NonCommercial 4.0 International (CC BY-NC 4.0)

Credit: The practical grocer : a manual and guide for the grocer, the provision merchant, and allied trades / by W.H. Simmonds ; with contributions by specialists, trade experts, and members of the trades ; illustrated by a series of separately-printed plates. Source: Wellcome Collection.

Provider: This material has been provided by The University of Leeds Library. The original may be consulted at The University of Leeds Library.

307/346 (page 249)

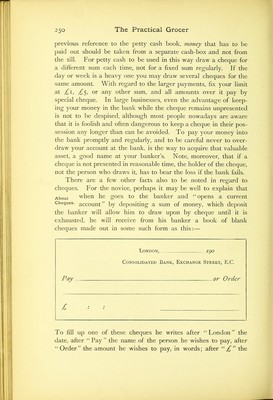

![in the order of their being posted, with each day’s check dated by adding a larger slip or check having on it the date of the day they are made out. When an article is returned it should be credited opposite the item charged. Thus, in drawing up an itemized state- ment there is a saving of labour by omitting this item. In the folio column are placed the salesmen’s numbers. At the end of the business year the accounts in this ledger are inventoried—making two lists—i.e. O. K. list and a doubtful list. The doubtful list is not considered in the resources when balancing the books. The doubtful list is balanced into a “suspended” ledger. For accounts kept in this form a perpetual ledger would be a great convenience. A diary is also kept, in which bills to be paid or other re- minders are entered. Bills for payment are entered on the page, bearing' a date a day or two previous to which they are to ° 1 r . ] A Diary. be paid. The discount to be taken is given, and when the ledger is to be referred to for goods returned, &c., a cross check is made. Statements are made up for payments from this book, and cheques drawn from the statements, which, if desired, may have a receipt attached, to be signed and returned. Such a diary as that above referred to may also usefully con- tain special pages for (a) memoranda of running contracts, showing date, article, and terms of contract; (/>) memoranda of goods brought forward, showing date or order, particulars, and dates for delivery. Other uses to which it may be put will readily occur in the course of business. 19. THE BANK—CHEQUES AND BILLS A word or two now regarding bank matters. We assume, of course, that the trader has not commenced business without opening a bank account. There are many advantages Pay by in possessing such an account; one, which is not the Cheiue- least, being that the use of cheques denotes the business man. The account kept by the bank itself, and the balancing of the pass- book therewith, constitute a useful safeguard and a permanent record. It is an excellent plan to make a hard-and-fast rule to pay all money received into the bank, and to pay out all outgoings over a certain amount by cheque. As we have explained in a](https://iiif.wellcomecollection.org/image/b21505949_0001_0307.jp2/full/800%2C/0/default.jpg)